The Biden Administration issued a final regulation and a new IRS notice on October 11, 2022, which eliminate the Affordable Care Act’s (ACA) “family glitch” beginning on January 1, 2023. The “glitch” refers to the fact that the ACA’s current affordability standard is based on what a single person pays for employer-sponsored coverage in all circumstances. This results in many people with employer-sponsored group health insurance paying far more for family coverage than the ACA’s coverage affordability threshold (9.5% of their household income, as adjusted annually for inflation).

Under this final regulation, if the employee’s cost for dependent coverage exceeds the ACA’s affordability threshold, then the affected dependents may be eligible for subsidized coverage through an exchange. The accompanying IRS notice allows employers to amend their Section 125 Cafeteria Plans to permit eligible dependents to drop their group coverage midyear in favor of subsidized individual exchange coverage.

Importantly, the final rule makes it clear that this change will not affect the coverage affordability requirements for applicable large employers (ALEs) subject to the ACA’s employer shared responsibility provisions (i.e., the employer mandate). The general rule that ALEs offer their full-time employees affordable coverage and the associated affordability safe-harbors remain in place. ALEs will NOT be required to offer affordable coverage to dependents.

The preamble to the final rule also explicitly states that the policy change will not impact ACA reporting for either ALEs or health insurance issuers. It remains unclear how the IRS and the health insurance exchanges will verify the cost of employer-sponsored dependent coverage or if an employee has an affordable offer of employer-sponsored coverage based on their family income.

The regulation does explain that the Biden Administration intends to:

- Revise the Exchange application on HealthCare.gov in advance of Open Enrollment for the 2023 plan year to include new questions about employer-sponsored coverage for family members;

- Revise the list of information consumers need to gather from an employer about the coverage being offered;

- Provide resources and technical assistance to State Exchanges that will need to make similar changes on their websites and Exchange application experiences;

- Provide training on the new rules to agents, brokers, and others who assist applicants so applicants will better understand their options before enrolling, including the trade-offs if applicants are considering splitting their family between exchange-based and employer-sponsored coverage; and

- Consider direct outreach to specific consumers who previously applied for subsidized coverage, were denied, but might benefit from the new rules.

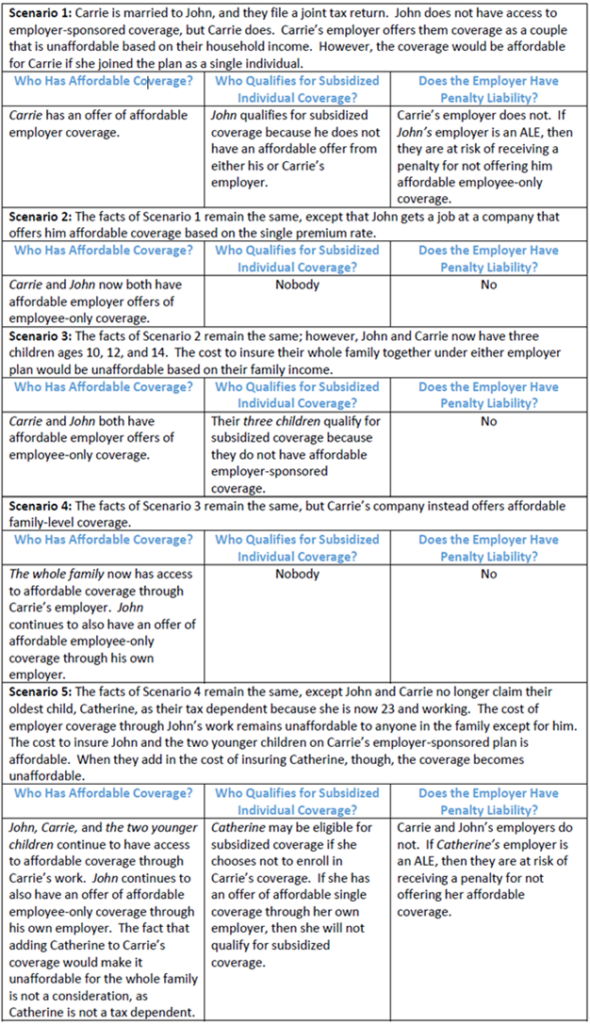

Who Could Qualify for Subsidized Exchange Coverage?

The regulation provides several examples of who could now qualify for a premium tax credit based on the new formula for assessing affordability of employer-sponsored coverage. The examples cover multiple complex situations, and we have summarized the most relevant scenarios in the following chart:

Additional Provisions of the Rule

The final regulation also makes related changes to the definition of “minimum value” coverage. As with the affordability rules, these revisions will consider family coverage when determining if a plan provides minimum value for dependents. The rules also codify long-standing guidance establishing that if a plan does not provide substantial coverage for inpatient hospital care and physician services, then it does not meet the minimum value standard.

Finally, the preamble to the final rule addresses concerns about how consumers will determine if coverage offered through a Qualified Small Employer Health Reimbursement Arrangement (QSEHRA) or through an employer-based Individual Coverage Health Reimbursement Arrangement (ICHRA) is affordable according to the new standards. The regulation states that because the affordability standard for QSEHRAs is set by federal statute, change here cannot be made without Congressional action. The IRS does intend to work with HHS on new guidance concerning ICHRA affordability assessments.

Related IRS Guidance

If an employer’s open enrollment period aligns with the annual exchange open enrollment period, then it will be simple for qualified individuals to decline group coverage and enroll in subsidized individual coverage through an exchange. However, the IRS has published Notice 2022-41 to address the complications that could arise under this final rule when an employer’s plan year does not correspond with the exchange’s open enrollment period.

In most cases, individuals who enroll in an employer-sponsored medical plan can only drop their coverage midyear if they have a “qualifying event.” This is due to the Section 125 Cafeteria Plan regulations that allow employees to pay for medical coverage on a pre-tax basis. Right now, a spouse and/or dependent children realizing they may be eligible for subsidized exchange coverage is not a qualifying event. This IRS Notice amends the existing Section 125 rules related to qualifying events so that employers with non-calendar plan years can now include this scenario as a qualifying event within their Section 125 plan documents. Of note, the existing Section 125 regulations already permit employees to prospectively revoke their election for employer-sponsored coverage midyear in order to enroll in exchange-based coverage during the annual open enrollment or if they become eligible for a special enrollment period.

According to the new guidance, employers with non-calendar year plans can now allow employees to revoke their family-level (non-health FSA) medical coverage as long as:

- At least one of their dependents wants to enroll in exchange-based coverage, either during the exchange’s open enrollment period or because the dependent is eligible for a special enrollment period through the exchange.

- And, the dependent(s) intend to enroll in exchange-based coverage that starts no later than the day after their coverage under the employer-sponsored plan ends. If the employee doesn’t also enroll in exchange-based coverage, they cannot revoke their own employer-sponsored coverage midyear. They, and any other individuals they’re covering who don’t enroll in coverage through an exchange, will need to maintain enrollment in the employer’s plan.

Employers can rely on an employee’s attestation as proof that their relative has enrolled or will enroll in exchange-based coverage. Employers are not required to allow these election changes. However, if they wish to permit the changes, they must:

- Inform employees of their right to make a change in accordance with the new rule, and

- Adopt a formal plan amendment on or before the last day of the plan year in which the election changes are allowed. This amendment may be made retroactively to the first day of the plan year* — meaning that election changes can technically be permitted before an amendment to the Cafeteria Plan document is made. Plans cannot be amended to allow an actual election of coverage to be revoked on a retroactive basis.

What Employers Need to Do

Moving forward, employers need to be aware of the change to the affordability standard for family coverage, be prepared to communicate with employees about the new rule, and be very clear about the exchange’s open enrollment deadline.

Additionally, it is more imperative than ever that ALEs ensure they are offering affordable, minimum value coverage to their full-time employees. While the ACA’s affordability requirements under the employer mandate (and associated penalty liability) continue to only apply to the employer’s lowest-cost offer of self-only, minimum value medical coverage, the existence of the new regulation means that more employees will seek exchange-based coverage. With more employees participating in the exchange, the likelihood that an ALE will receive a penalty when they fail to offer employees affordable coverage increases, too.

Finally, employers with non-calendar plan years should consider adopting the changes to their Section 125 Cafeteria Plan that this new IRS guidance permits. MZQ will help all our Compass and Compass Plus clients adopt these changes in advance of the regulated deadline.

*For plan years beginning in 2023, an extra year is permitted to complete the amendment (e.g., if a plan year begins April 1, 2023, the plan has until March 31, 2025 to complete the amendment).